Meeting global infrastructure needs over the coming decades will require significant investment. Projections estimate a $64 trillion funding gap over the next 25 years, underscoring the limitations of public financing and the need for complementary sources of capital.1

Private infrastructure has increasingly filled this role, emerging as a critical segment of global private markets. Since 2000, assets under management (AUM) have compounded at

an annual rate of 24%, surpassing $1.5 trillion in 2024 and accounting for nearly 10% of total private markets AUM (Figure 1). The asset class continues to expand rapidly, valued for its resilience, inflation protection and diversification benefits.

What is infrastructure?

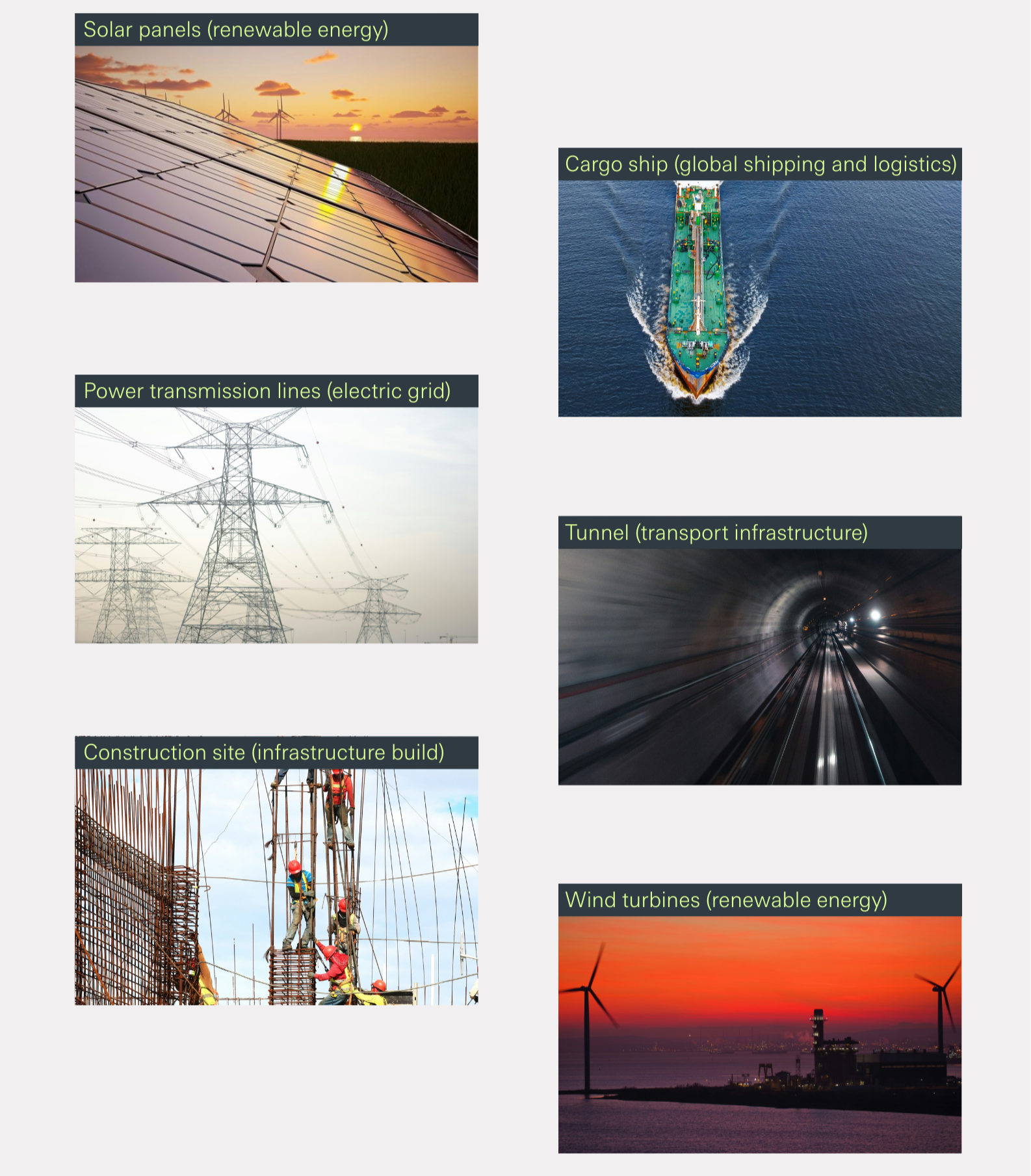

Infrastructure encompasses the systems and assets that deliver services and products to support economies and societies. This includes areas such as power and renewables, utilities, transportation, digital and social infrastructure, and the investable universe continues to expand around key global themes:

- Energy transition: Renewables, energy storage, distributed generation, transmission and EV.

- Digital and AI revolution: Data centers, fiber networks, wireless towers and small cells.

- Urbanization and modernization: Smart transportation and logistics, urban mobility and decarbonized freight solutions.

- Sustainable communities: Healthcare, education and environmental services like water treatment and waste management.

Why infrastructure?

Several structural features explain the resilience and appeal of infrastructure.

- Downside protection: Infrastructure assets provide essential services with relatively inelastic demand. Many operate under long-term contracts or regulated frameworks, insulating revenues from market swings and shocks (Figure 2).

- Diversification benefits: Infrastructure returns have historically exhibited low correlation with traditional listed investments (Figure 3).

- Stable returns and yields: Investments are typically backed by tangible assets and long-term contracts, generating predictable cash flows and high operating margins. These features generate steady income and reduce return volatility relative to other asset classes (Figure 4).

- Inflation hedge: Many infrastructure assets benefit from inflation-linked user pricing or regulated tariff structures, enabling operators to pass rising costs to end-users. Combined with essential demand, this provides resilience in inflationary environments (Figure 5).

Risk and return

Infrastructure assets can vary widely in geography, sector, project stage, revenue framework, cash flow profile and

risk level. These differences shape return expectations and determine positioning along the risk/return spectrum. The following broad categorizations have formed as the market has developed (Figure 6):

- Core: Equity in mature, essential businesses—like utilities, transport networks or communication systems—that people rely on every day. These businesses usually face little competition owing to regulation or high costs of entry, and generate steady cash flows through long-term contracts. Returns come mainly from income, with modest growth potential.

- Core-plus: Similar to core, but with more variability and growth potential. These could involve adding new projects to an existing platform, or a “build-to-core” strategy, where investors take on some development risk before the asset matures. Returns combine income with more upside from capital appreciation.

- Value-add: Assets that require meaningful growth, expansion or repositioning. Cash flows are less predictable, with shorter contracts. Returns come mostly from appreciation as the asset grows in value.

- Debt: A lower-risk way to invest in infrastructure. Instead of owning assets, investors earn income through interest payments on loans made to infrastructure projects or companies. Because the payments are typically fixed or floating coupons, returns are steadier and more predictable, with less potential for upside.

Real world examples

Investment structures

Investors can access infrastructure through four main channels:

- Closed-ended funds (also known as commingled or primary funds) are investment vehicles in which an investor—typically a limited partner (LP)—commits capital upfront. Depending on their entry point, investors may have varying levels of visibility into the underlying portfolio. As the general partner (GP) identifies investment opportunities, LPs are required to fund portions of their committed capital. These investments are generally held for a period of 10-15 years. Because capital is called and returned unpredictably, managing liquidity can be challenging for investors. Nevertheless, by committing to multiple funds across different vintages, investors can achieve relatively steady cash flow profiles from their private infrastructure portfolios. Owing to high minimum commitment requirements, access to closed-ended funds is usually limited to institutional and high-net-worth investors.

- Co-investments allow investors to invest alongside a GP—often with reduced fees. This can help investors tilt their portfolios to desired exposures, average down fees and gain critical insights into the strength of the GP and their investment team. Co-investors must move quickly and often deploy specialized deal teams.

- Secondaries involve acquiring interests in an existing closed-ended fund, frequently at a discounted price, or in asset(s) already managed by a GP. These transactions can be initiated either by the GP or a LP. Since buyers enter at a later stage in the fund’s life, they typically gain exposure to a more mature, diversified portfolio or asset—allowing for faster capital deployment and potentially quicker returns. Participating in secondaries requires specialized expertise.

- Evergreen funds (also known as semiliquid structures) are gaining momentum as a more convenient and efficient way to access infrastructure. While open-ended funds have long played a role in infrastructure investing, evergreen vehicles offer a distinct format that combines continual capital deployment with periodic liquidity, helping to address some of the limitations of traditional closed-ended structures. These funds are increasingly being adopted by investors seeking more immediate exposure, diversification and greater flexibility.

Conclusion

Infrastructure is a fast growing asset class that can offer investors stable returns, a potential inflation hedge and diversification. At the same time, its investable universe continues to evolve, shaped by transformative themes such as the energy transition, digital connectivity and sustainable development. For investors, partnering with a GP that combines global reach with operational expertise is key to unlocking new opportunities.

1 Robert Gilhooly, Tettey Addy and Mark Bell, How Large Are Global Infrastructure Needs? Aberdeen Global Macro Research, Aberdeen Investments, June 5, 2025, https://www. aberdeeninvestments.com/en-us/investor/insights-and-research/how-large-are-global-infrastructure-needs-us.